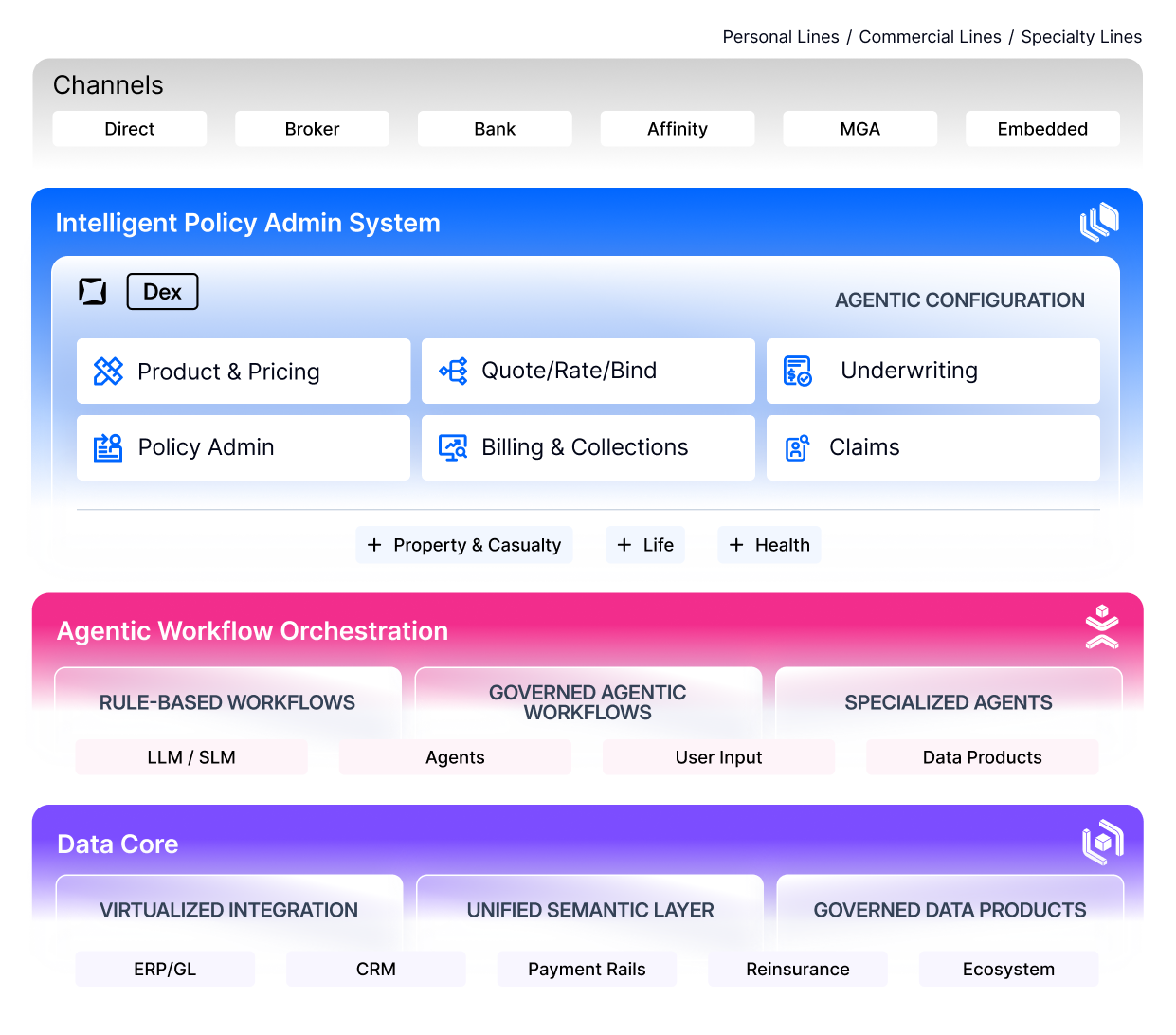

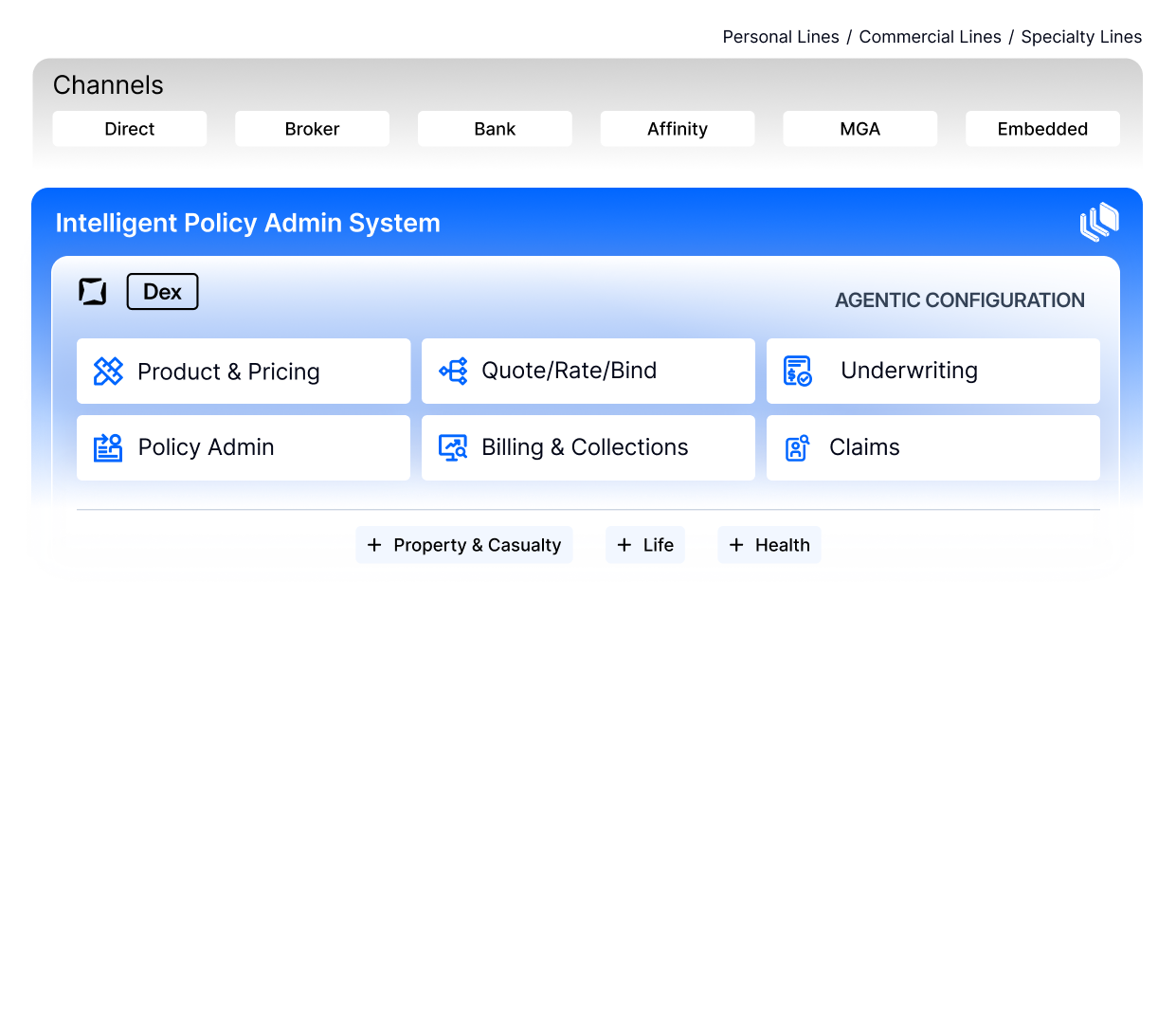

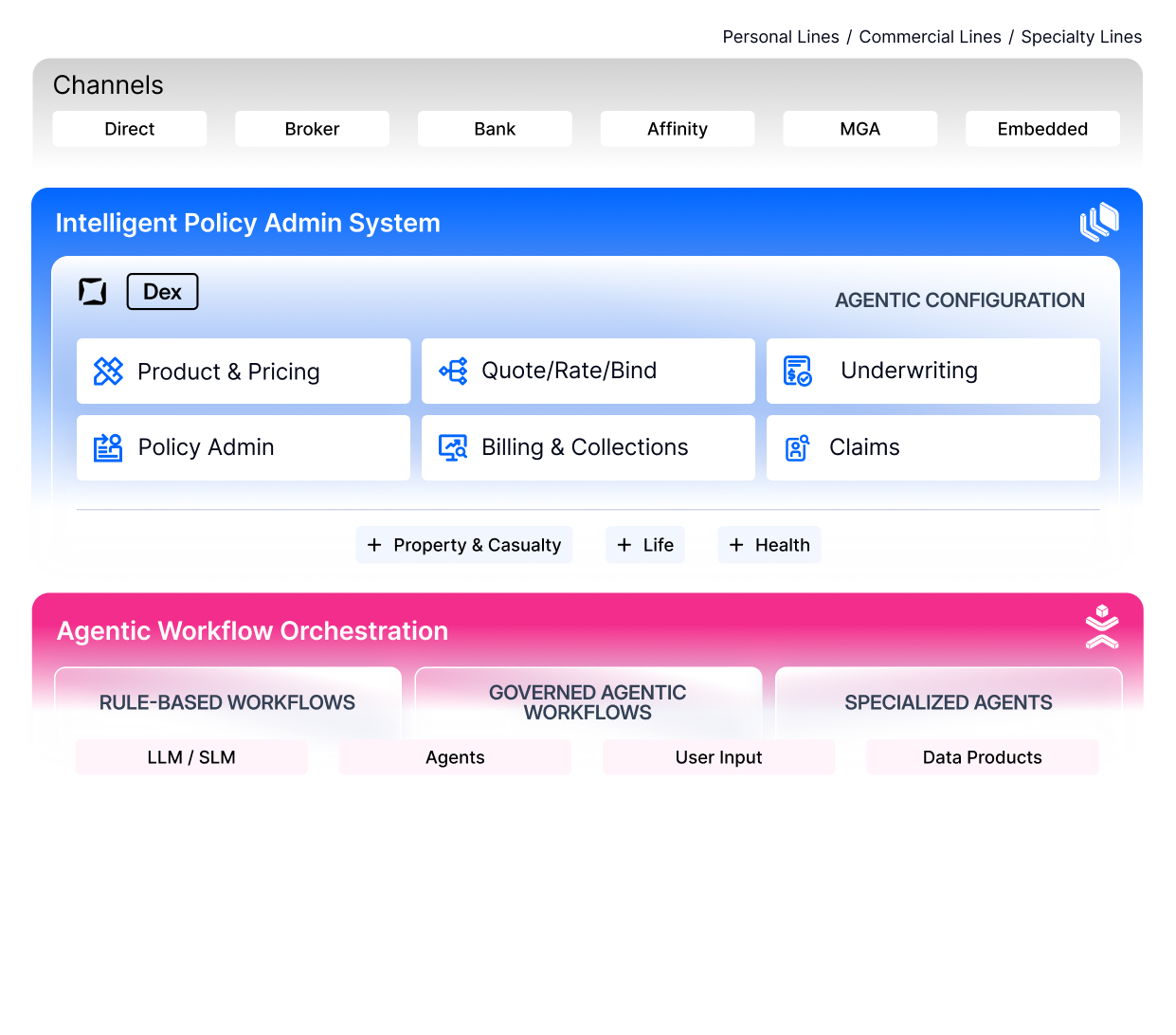

Intelligent Policy Admin System

A composable layer for policy administration, origination, and claims, across channels, lines of business, and the legacy PAS estate. Click each layer to step through the architecture.

Consistent product, pricing, and customer journeys across every channel. Integrates with your existing channel capabilities or replaces them with FintechOS-native ones, with personalization applied at the channel-and-customer level rather than per silo.

End-to-end policy administration across the lifecycle, unified across product lines (P&C, life, health, pet, and specialty) and customer segments. Configured through Dex, the AI copilot for natural-language authoring against a governed schema. Out-of-the-box solution accelerators across each line, fully configurable to your wordings, rates, and underwriting appetite.

The runtime that coordinates AI agents, human practitioners, and structured business processes in one governance framework: BPMN-aligned, deterministic at the process level, agentic at the task level. Agent actions are audit-traceable and policy-constrained, with human-on-the-loop controls where decisions warrant them. That's what makes agentic AI governable in regulated environments.

Data Core resolves the fragmented PAS estate without forcing physical consolidation: virtualising access to every legacy PAS, CRM, payment rail, reinsurance platform, ERP/GL system, and external service through a unified semantic layer. Agents and humans reason over one coherent, governed view of the customer and the policy, rather than a patchwork of disconnected systems.